HOUSTON–(September 24, 2018)– Contango ORE, Inc.(“CORE” or the “Company”) (OTCQB: CTGO) is pleased to announce that Peak Gold,LLC (“the Peak Gold Project”), a joint venture between the Company’s wholly owned subsidiary CORE Alaska, LLC (“CORE Alsaka”)and Royal Alaska, LLC (“Royal Alaska”), a wholly owned subsidiary of Royal Gold Inc, has received its Preliminary Economic Assessment (“PEA”) of its Main Peak and North Peak resource areas near Tok, Alaska. ThePEA presents a robust open pit mining operation with attractive economics atbase case gold and silver prices. All results presented herein are on a 100%Peak Gold basis.

PEA Highlights

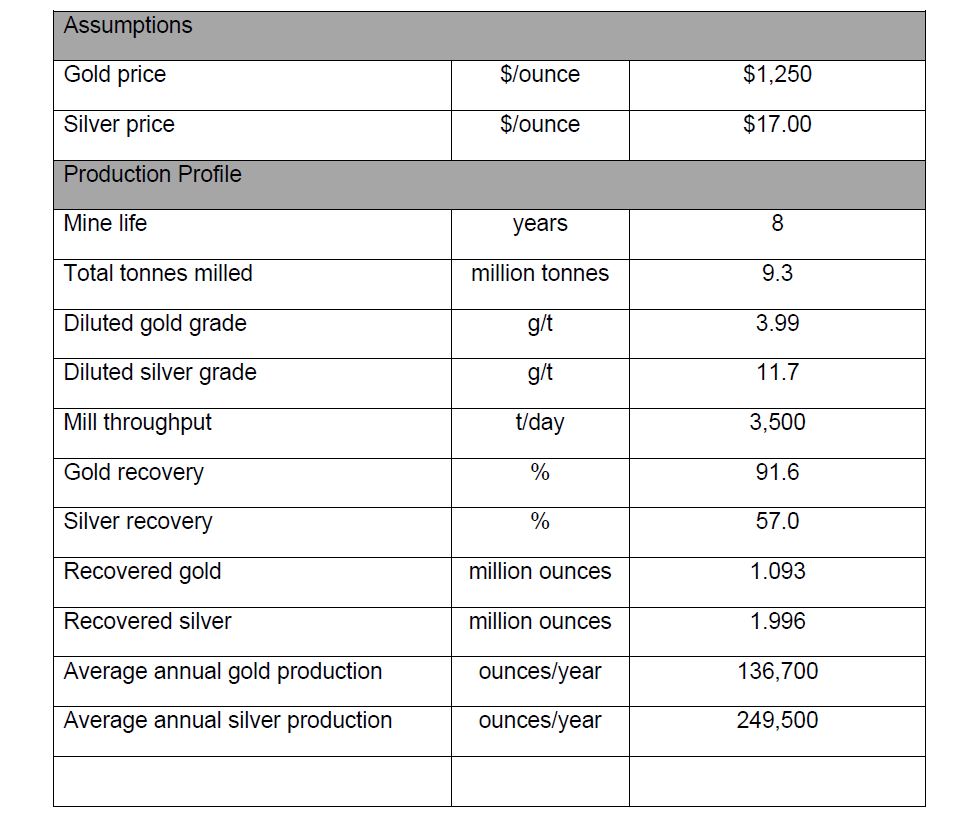

Highlights of the PEA results,assuming base case metal priceparameters of US$ 1,250 per ounceof gold and US$ 17.00 per ounceof silver and net to Peak Gold of which the Companyowns 60%, include:

· Pre-tax NPV5% ofUS$ 393 million and IRR of 37.0%;

· After-tax NPV5%of US$ 283 million and IRR of 29.1%;

· Mine life ofeight years with a 24-month pre-production period;

· 9.3 milliontonnes processed at an average grade of 3.99 g/t gold and 11.7 g/t silver;

· Averagemetallurgical recoveries of 91.6% for gold and 57.0% for silver;

· Life of minerecovered gold of 1.093 million ounces and 1.996 million ounces of silver;

· Life of minestrip ratio of 3.9 tonnes of waste to tonnes of material processed;

· Life of minetotal cash cost of US$ 428 per ounce of gold recovered, and US$ 470 per ounceof gold recovered including sustaining capital;

· Life of mine capital cost of US$ 340million, consisting of US$ 294 million of initial development capital, andsustaining capital and closure costs of US$ 46 million; and

· After-tax paybackperiod for initial development capital of approximately 2 years.

The PEA was prepared by JDS Energy and Mining Inc.(“JDS”), of Vancouver, British Columbia, Canada.

Brad Juneau, the Company’s CEO said, “This first PEApertains only to Peak Gold’s Main Peak and North Peak resource areas. Therobust economic returns are a result of the deposit’s high grade, low strip ratio, shallow depth of the resource, and access to infrastructure. Establishing an economic project in the Peak area is a great start to realizing the ultimatevalue of Peak Gold’s assets which includea large acreage position outside of the Peak area with significant exploration potential. Royal Gold will bemaking a presentation on the Preliminary Economic Assessment at the Denve rGold Forum on Monday September 24, 2018, whichwill be availableon the company’s website at www.contangoore.com by Tuesday, September 25, 2018.”

PEA Overview

The PEA considers a conventional truck and shovelopen-pit mining operationcovering the North, Main and West Peak deposits, feeding a 3,500 tonne per day processing plant with two-stage crushing, grindingand a carbon in leach (“CIL”) recoverycircuit, with production of gold-silver doré bullion on site. The PEA is based on an updateof the mineral resource estimate1for the Peak and North Peak deposits previouslyannounced by CORE in our June 2, 2017 press release.2

PEA Parameters and Economic Results

The main parameters and results of the PEA are summarized in the following table:

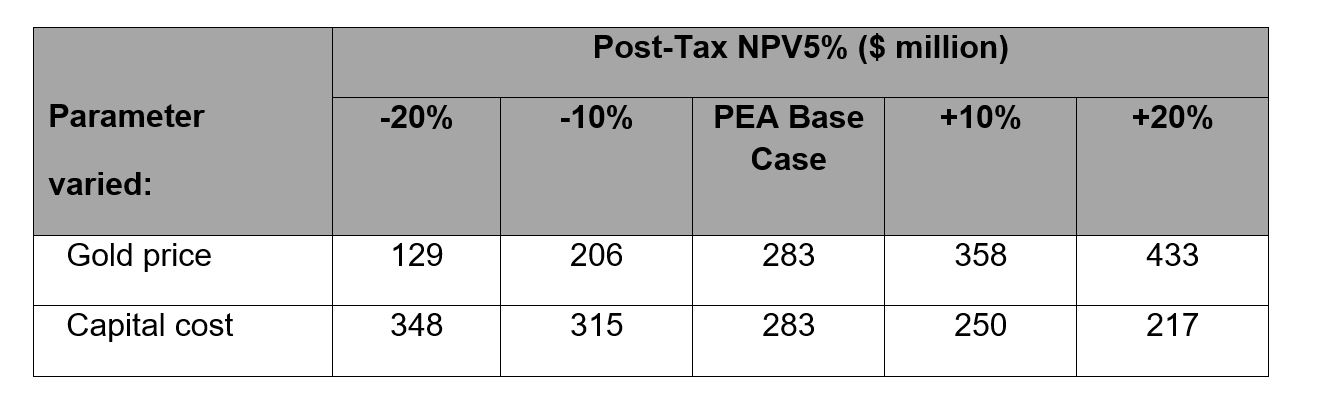

Economic Sensitivities

Sensitivity of the estimated post-tax NPV5% to changes to significant value drivers is shown below:

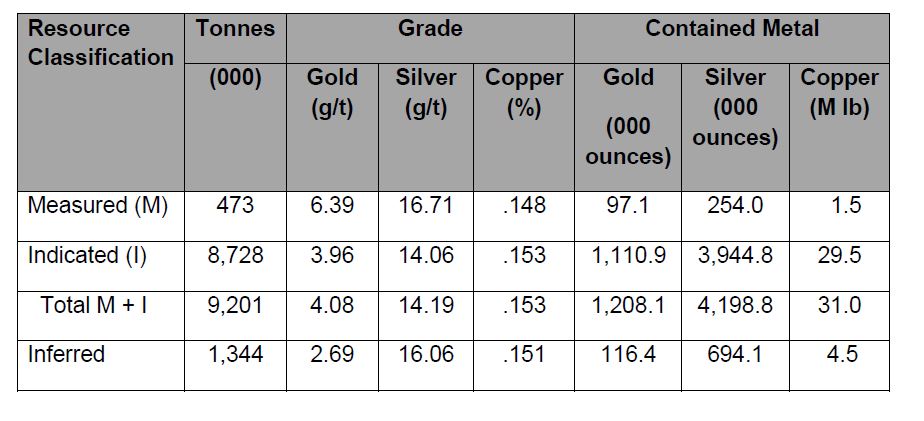

Mineral Resource

The PEA is based on the resource estimate prepared by Independent Mining Consultants, Inc. and reported by CORE on June 2, 2017. The resource estimate was updated using operating costs, pit slope estimates and metal recoveries consistent with the PEA parameters in September of 2018,resulting in a revised resource estimate, which is summarized in the table below:

The estimates of measured and indicated resources assumed metal prices of $1,400 per ounce gold and $20.00 per ounce silver for development of the pit shell. The cutoff grades used to define resources were 0.74 g/t gold equivalent for the Main Peak deposit and 0.66 g/t gold equivalent for the North Peak deposit.

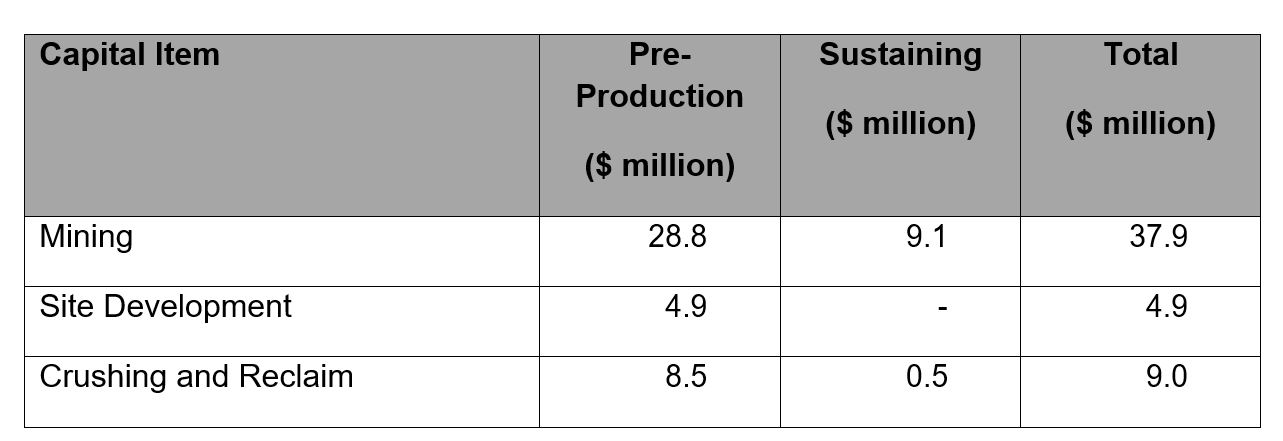

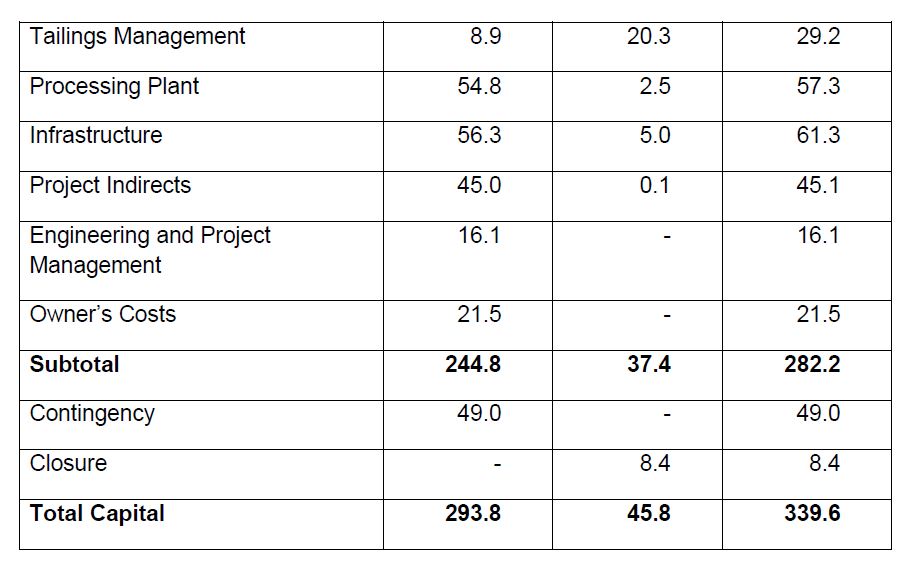

Capital Costs

The PEA is based on a capital cost summary with an estimated accuracy of +/- 30%, which is shown in the table below:

Pre-production capital reflects the required investment to develop the Project through to production. Sustaining capital is for theentire life of mine and includes equipment, spare parts, expansion of thetailings management facility, water management and closure costs.

Mining

The PEA assumes conventional open pit truck and shovel mining, and production designed to achieve a processing rate of 3,500 tonnes per day. The average mining rate assumed by the PEA is 15,000 tonnes per day of total material mined, with a maximum of 22,000 tonnes per day occurring in years 3 through 6.

The mine designassumed by the PEA will consist of two pits, with a mining sequence intended to maximize grade in the early years, reduce stripping requirements and maintain the processingfacility at full production capacity. Operations would begin at the North Peak deposit and transition in year three to a single pit comprising the Main and West Peak deposits forthe remainder of the mine life.

The primary owner-operated diesel mine fleet is designedto consist of 64 tonne capacity haul trucks, 7.0 m3 front shovels, a 7.0 m3 front end loader and 127 mm diameter drills. The ancillary minefleet would consist of track dozers, graders, wheel dozers and water trucks.

Processing

The PEA assumes mineralized material would be processed using a two-stage crushing circuit, a two-stage grinding circuit, and a CIL circuit. Run of mine material would be fed to a primary jaw crusher, after which oversize material would be fed to a secondary cone crusher. Fine mill feed wouldreport to a primary rod mill to be mixed with cyanide,cement and milk of lime. The feed mixture would then proceed to a secondary ball mill, after which it would enter a grindingthickener followed by a five-stage leach/adsorption circuit. Gold and silver would be recovered from the leach solution and smelted in an inductionfurnace to produce doré bullion.

The PEA assumes CIL tailings would be pumped to a tailings thickener to remove process water and recover free cyanide for reusein the plant. Thickened tailings would be detoxified and then pumped to the tailings management facility (“TMF”) for storage. The TMF would be lined with asynthetic geomembrane liner and wouldhave foundation and underdrain systemsto minimize and control potential seepage. Thetailings embankment would be raised continuously over the mine life and wouldbe designed to allow capacity for future expansion, if required.

Project Infrastructure

The PEA assumes general infrastructure for the Project would support operations on a 24 hour per day, seven day per week basis. Major infrastructure items would include:

· Site access road connecting to the Tetlin Village road and the Alaska Highway, with upgrades to the existing site access road over a 10-kilometer distance;

· Haul roads for waste and mill feed materials sized to accommodate 65 tonne trucks;

· Maintenance,warehouse, administration, laboratory, security and first aid buildings;

· Plant facilities, including the crushing and grinding circuit, conveying equipment, and refinery;

· Ancillary facilities, including a truck shop, explosives storage and fuel storage;

· Power line from Delta Junction to a site substation (approximately 160 kilometers) to supply a total connected load of 8 MW;

· Camp accommodations in Tok for the portion of the workforce that does not come from Tok, Tetlin and the surrounding areas;

· Water supply and management system to minimize water discharge from the site;

· Lined TMF, constructed with an initial capacity for two years of tailings, with staged construction in subsequent years to increase storage capacity as required; and

· Waste rock storage areas to allow segregation of waste depending on its characteristics.

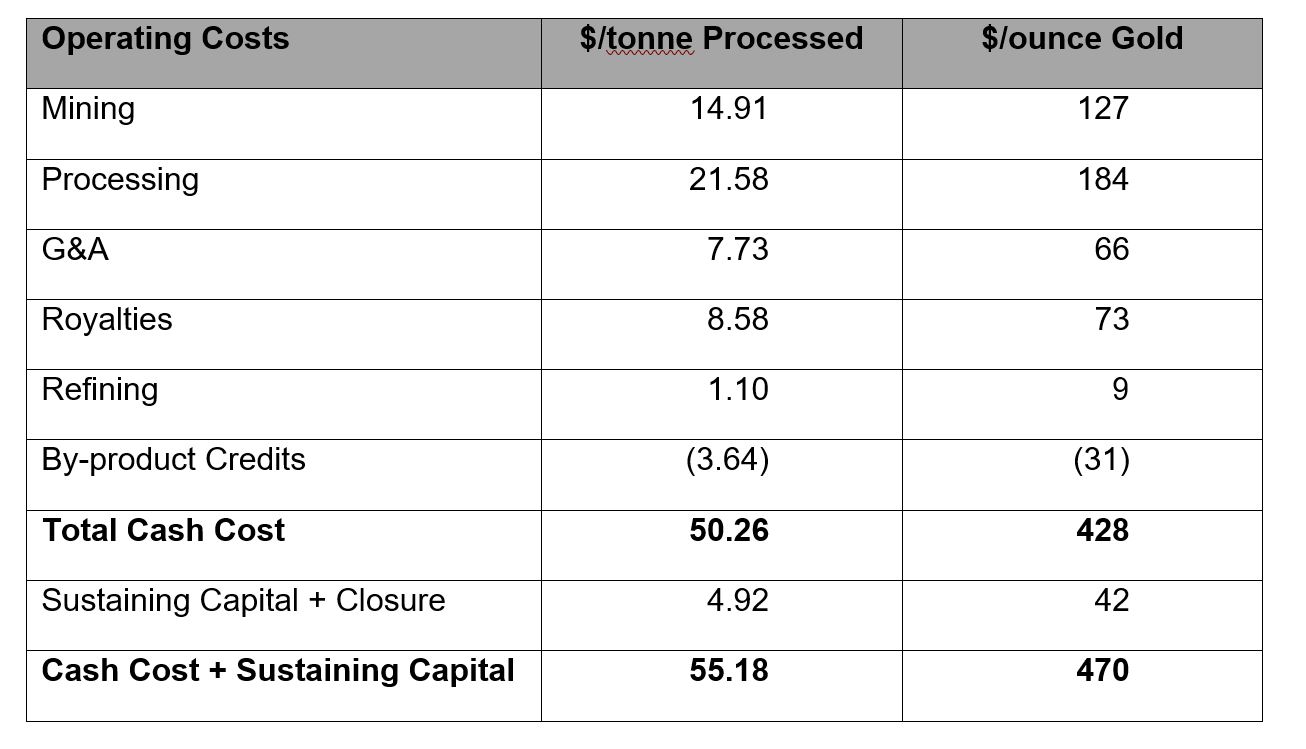

Operating Costs

The PEA is based on assumed life of mine operating costs by activity area, as shown in the table below.

Under the mineral lease for the Project, Peak Gold would pay a production royalty based on net returns of mineral production from the lease area. The production payment rates under the lease for precious metals are currently 2.25% of net returns for the first four years of production,3.25% of net returns for years five through seven inclusive, and 4.25% of net returns for year eight and any following years. These royalty rates can be increased at the option of the royalty holder to 3.0%, 4.0% and 5.0%, respectively, with the payment of an additional $150,000, $300,000 and

$400,000 to Peak Gold for each respective royalty period, before July 15, 2020.

In addition, Peak Gold would pay a royalty to Royal Gold at a rate of 3.0% of net smelter returns on mineral production from the lease area underlying the project considered in the PEA.

Permitting

Peak Gold holds the required permits and approvals to continue exploring the areas comprising the Project. The collection of baseline water quality data, material characterization analysis and wetlandsdetermination has progressed since 2012. A more comprehensive baseline data collection program is being contemplated for 2019.

Project Enhancement Opportunities

Several opportunities have been identified that could enhance the project considered by the PEA, including:

· Expansion of the mine through delineation or development of additional mineral resources;

· Pit slope steepening to improve the assumed waste to mill feed strip ratio;

· Optimization of the assumed mine plan and development schedule; and

· Potential recovery of copper.

The results of the PEA are preliminary in nature and are based on various assumptions. These assumptions may be affected byenvironmental, permitting, legal, title, taxation, socio-political, market or other relevant factors, including changes in metal prices. In addition, nodecision has been made by Peak Gold to proceed with the mine plan described inthe PEA. A decision to proceed with the mine plan would requirefurther economic study.No decision has been made byPeak Gold to proceed with a further economic study. Accordingly, there is nocertainty that the results of the PEA would be realized should Peak Gold decideto proceed with the mine plan described in the PEA at any point in the future.

ABOUT PEAK GOLD

Peak Gold is a joint venture betweenRoyal Alaska and CORE Alaska,a wholly-owned subsidiary of CORE. Peak Gold holds a 675,000 acre lease with the NativeVillage of Tetlin and an additional175,000 acres of State of Alaska miningclaims, all locatednear Tok, Alaska,on which Peak Goldexplores for minerals. CORE Alaska holds a 60% membership interest in Peak Goldand Royal Alaska holds a 40% membership interest in Peak Gold and is themanager of the joint venture. Royal Gold also holds a 13.2% equity interest inCORE, and royalties of 3.0% of net smelter returns on mineral production fromthe lease and certain State of Alaska mining claims held by Peak Gold and 2.0%of net smelter returns from certain other State of Alaska mining claims held byPeak Gold.

ABOUT CORE

CORE is a Houston-based company that engages in the exploration inAlaska for gold and associated minerals through Peak Gold, its joint venturecompany with Royal Alaska. Additional information can be found on our web pageat www.contangoore.com.

FORWARD-LOOKING STATEMENTS

This press release contains forward-looking statements regardingCORE that are intended to be covered by the safe harbor “forward-lookingstatements” provided by the Private Securities Litigation Reform Act of 1995,based on CORE’s current expectations and includes statements

regarding future resultsof operations, qualityand nature of the asset base, the assumptions upon which estimates are based and otherexpectations, beliefs, plans, objectives, assumptions, strategies or statementsabout future events or performance (often, but not always, using words such as “expects”, “projects”, “anticipates”, “plans”, “estimates”, “potential”, “possible”, “probable”, or “intends”, or stating thatcertain actions, events or results “may”, “will”, “should”, or “could” betaken, occur or be achieved). Forward-looking statements are based on currentexpectations, estimates and projections that involve a number of risks anduncertainties, which could cause actual results to differ materially fromthose, reflected in the statements. These risks include, but are not limitedto: the risks of the exploration and the mining industry (for example,operational risks in exploring for, developing mineral reserves; risks anduncertainties involving geology; the speculative nature of the mining industry;the uncertainty of estimates and projections relating to future production,costs and expenses; the volatility of natural resources prices, includingprices of gold and associated minerals; the existence and extent ofcommercially exploitable minerals inproperties acquired by Peak Gold; potential delays or changesin plans with respect to explorationor development projects or capital expenditures; the interpretation ofexploration results and the estimation of mineral resources; the loss of keyemployees or consultants; health, safety and environmental risks and risksrelated to weather and other natural disasters); uncertainties as to theavailability and cost of financing; inability to realize expected value fromacquisitions; inability of our management team to executeits plans to meet its goals; and the possibility that governmentpolicies may change or governmental approvals may be delayed or withheld, includingthe inability to obtain anymining permits. Additional information on these and other factors which could affect Peak Gold’s exploration program orfinancial results are included in CORE’s other reports on file with theSecurities and Exchange Commission. Investors are cautioned that anyforward-looking statements are not guarantees of future performance and actualresults or developments may differ materially from the projections in theforward-looking statements. Forward-looking statements are based on theestimates and opinions of management at the time the statements are made. COREdoes not assume any obligation to update forward-looking statements shouldcircumstances or management’s estimates or opinions change.

1 The PEA was preparedin accordance with Canadian National Instrument 43-101 (NI 43-101). CORE is not subjectto regulation by Canadian regulatory authorities and no Canadian regulatory authority has reviewed the PEAor passed upon its accuracy or compliance with NI 43-101.The terms “mineralresource”, “measured mineralresource”, “indicated mineralresource” and “inferred mineral resource” as used in the resource estimate, the PEA and this press release are Canadianmining terms as defined in accordance with NI 43-101;however, these terms are not defined terms under the U.S. Securities and Exchange Commission’s (SEC’s) Industry Guide 7 and are normally not permitted to be used inreports and registration statements filed with the SEC. The estimation of measured resources andindicated resources involves greater uncertainty as to their existence and the legal and economicfeasibility of extraction than the estimation of proven and probable reserves.Conversion of mineral resources to proven and probable mineral reservesgenerally requires a further economic study, such as a preliminary feasibilitystudy. The PEA is not a preliminary feasibility study and does not support anestimate of proven and probable mineral reserves. Investors are cautioned not to assumethat all or any part of an inferred mineralresource exists or is economically or legally mineable. Investors arealso cautioned not to assume that all or any part of measured or indicatedresources will ever be converted into mineral reserves. In addition, the SECnormally only permits issuers to report mineralization that does not constitutemineral reserves as in-place tonnage of mineralized material and grade withoutreference to unit amounts of metal.

2 The “Main Peak” and “West Peak” deposits werepreviously referred to as the “Peak” deposit in the June 2, 2017 resourceestimate.

CONTACTS

Contango ORE, Inc.

Brad Juneau,(713) 877-1311 www.contangoore.com